Updated on 2 April 2025

6 minute read

Ever wondered why your super balance can go up and down? Your super's invested to help it grow, which means it's affected by market cycles. Here's how they work.

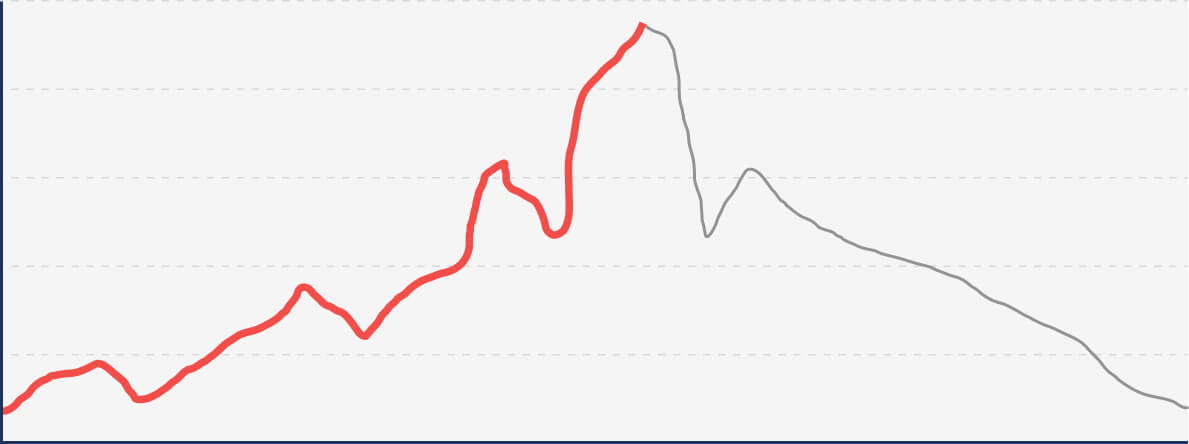

A market cycle is the pattern of a financial market's performance over a period of time. The stages of the cycle are defined by whether the market is rising or falling in value by any significant amount, and by how quickly that change in value happens.

Some people describe markets cycles as having a set number of clearly defined stages. But in reality, markets tend to generally experience periods of rising values (bull markets), highs (peaks), minor falls (corrections), big falls (crashes), and periods of falling values (bear markets). There's often not a clear pattern, especially while we're in the middle of the cycle.

Market cycles don’t just happen in the share market. Any type of asset you can buy and sell can have a market cycle, like property, bonds, and even gold. When we talk about markets and market cycles in this article however, we're talking about share markets.

There's no set amount of time the market spends in each phase. A crash might only last a few days, whereas a bull market can sometimes last for years.

A bull market is a pattern of investor optimism and rising prices, usually over a long period of time (months or years). Prices can still go up and down in this market. A bull market tends to last the longest of all the phases, sometimes for years at a stretch.

A market peak is when the share market reaches its highest point of value. There tends to be lots of small market peaks as prices rise in a bull market. But a market peak can also mean the final peak or high point before the beginning of a bull market. It's very difficult to know if a market is peaking until after it's happened.

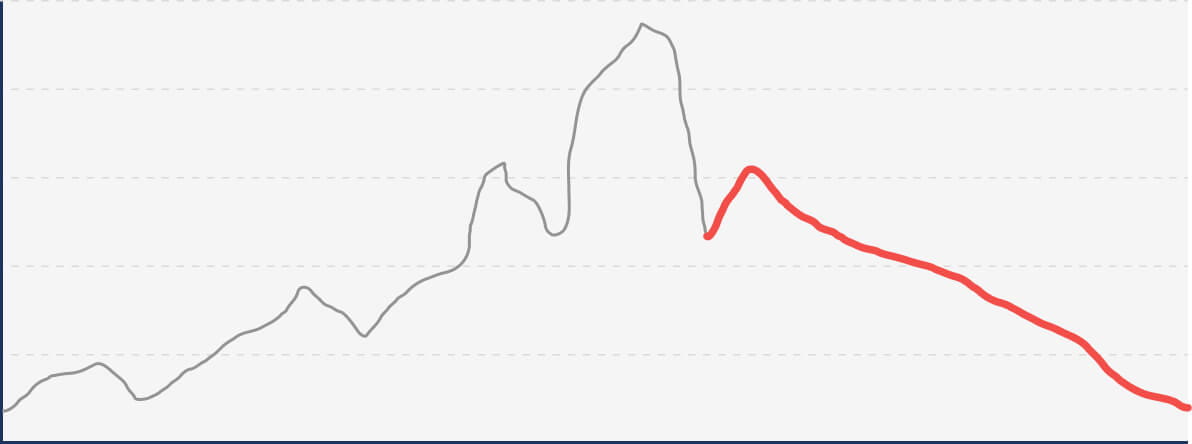

There's a general view that a market correction is when values fall between 10-20% from a recent market peak. Market corrections can happen when prices rise too quickly and become overvalued or overinflated. Often a correction will simply return (or correct) prices to their long-term market trends.

Like with market peaks, it's very difficult to tell whether a fall is a correction or a crash until the fall is over. And depending on how your super is invested, you could see the impact of a correction on your super balance. Bear in mind that a correction is a short-lived fall. It will often only last a number of weeks.

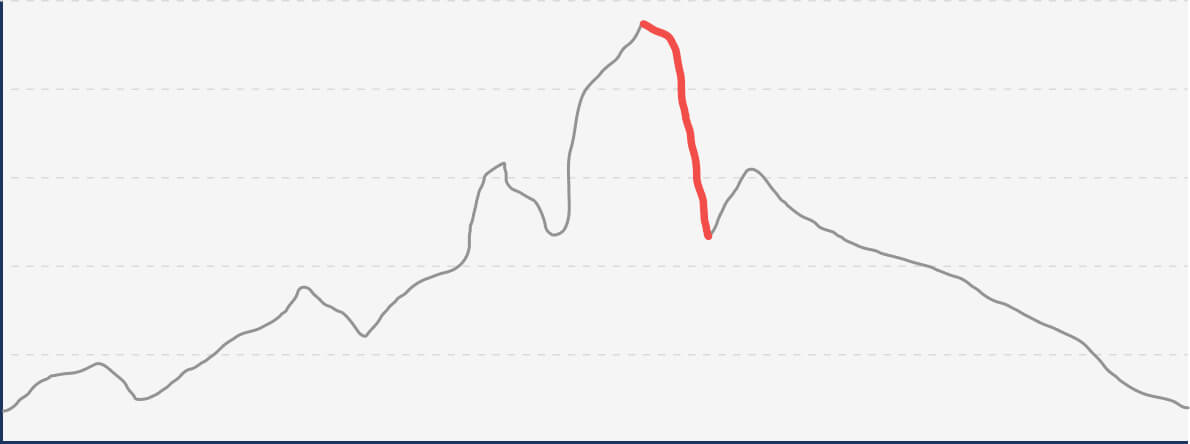

Generally, a share market is considered to have crashed when it drops by more than 20% in value from a recent peak, in a short period of time (usually measured in days).

When a market enters a period of falling values and investor pessimism, it's often called a bear market. Unlike a crash, in a bear market prices fall and continue to fall over a longer period of time. Bear markets often last for months. Like with crashes, the general rule is there needs to be a drop of more than 20% in market value from a recent peak.

Bear markets sometimes coincide with economic downturns or recessions, but they don't always. It's a period of time marked more by investor pessimism. When investors are pessimistic, more of them sell their investments and withdraw from the market. With less investors and less optimism in the market, prices tend to stay lower for longer.

How investors feel about the market can fuel market movements like bull and bear markets. But markets are affected by a much wider range of factors than sentiment. The following factors affect market behaviour as well:

All of these factors together make predicting market cycles extraordinarily difficult. So what can you do about your super, if you can't predict the market?

When your super is going up, that's great! But it can be difficult to know what to do or how to feel when your super goes down. There could be a number of reasons why your super balance is fluctuating.

As a first step, it's good to understand how your super's invested. And if you have an investment strategy for your super, use that to guide your decisions.

Remember, if you're not sure what to do, you could consider getting financial advice.

Different types of investors have different needs. If you're a member with us, you can get financial advice about your super account with us over the phone. We include the cost of advice with your membership.1

Diversification means spreading your investments out across a few different asset classes (like shares, infrastructure, or fixed income) at once. This strategy aims to limit the amount of exposure you have to the ups and downs of a single market. Diversifying means your super is likely to be less affected by market downturns. You can't eliminate this risk entirely, however.

Why diversify? Well, when one market you're invested in isn't doing too well, it'll only affect the part of your portfolio that's invested in that market. The trade-off is that if one particular market is doing well, only the part of your portfolio that's invested in that market will benefit.

Here are a few things to consider:

Your investment timeframe: how long you have to invest your money before you need to use it (for super, this is usually your life expectancy minus your current age). The longer your timeframe, the better positioned you are to take on riskier investments – if that's something you feel comfortable doing.

Your risk tolerance: this is how much risk you're willing to tolerate to get the level of returns you want. You should balance this against how much super you want to retire with, and how long you have to invest. If you're not willing to tolerate much risk, the trade-off could be lower returns that won't reach your retirement goals.

Your retirement goals: this is how much super you want to retire with. You'll need to factor in inflation and rising costs of living, as well as the kind of lifestyle you'd like to live in retirement.

Not sure how much you'll need to retire with? Check out our retirement planning calculator.

Test your inner investor and see what type of investment options may suit you best.

Take the quizDuring a recession, your super balance might decrease as share markets often fall. However, recessions are typically followed by periods of growth. By staying invested, you could be positioned to benefit from the recovery.

Market performance, like a correction or a bear market, can cause your super balance to drop in the short-term. But remember, your super is a long-term investment. Despite short-term fluctuations, the overall trend across all share markets has been positive over the long term.

There's no set period of time the market tends to spend in each part of the cycle, but there's a saying that markets go up the stairs, but come down the elevator. Values rise over a long period of time, but falls happen relatively quickly. Historically speaking, share markets have spent much more time in periods of rising values (typically years longer) than falling values.

When a market starts to recover from a period of decline, the cycle starts again.

It's not always clear which phase we're in, and the phase could change quickly at any time. It can also be hard to tell what part of the cycle we're in until it's over. For example, it's not clear whether a fall in values is a correction or a crash until it's finished happening.

The superannuation market has a slightly different definition to other markets. Whereas other markets are usually identified by the assets they trade (real estate or bonds, for example) the superannuation market refers to how much superannuation is invested across all markets. According to the Association of Super Funds of Australia, the total amount of superannuation invested in the market in September 2024 was $4.1 trillion.2

Want to learn more about how we're investing your super for the long term? Check out our investment options or read our latest investment update.

Learn about market volatility, how it can affect your super, and what you can do to help manage it.

3 min read

Learn the basics of investing your super to help you fund the lifestyle you want in retirement.

4 min read

Listen to our Head of Investment Strategy, Andrew Fisher, explain how his team builds portfolios that aim to grow retirement savings while managing risk.

18 min listen

1. Any advice given is by representatives of Sunsuper Financial Services Pty Ltd (ABN 50 087 154 818, AFSL 227867), wholly owned by the Trustee of ART. As representatives, they may recommend ART products from time to time. Please read the Sunsuper Financial Services FSG - individual for more info about that advice and how they’re paid.

2. ASFA, 2024, accessed on 24 February 2025 at https://www.superannuation.asn.au/