Updated on 15 April 2025

4 minute read

Find out what your super fees really pay for, and learn how to do your own superannuation fees comparison.

There are 2 main things to consider when thinking about your super fees:

The level of net investment returns you're getting

The amount of fees you're paying

The bigger the returns, the more your money grows. The more it grows, the more money you'll have to retire with.

But on the other hand, high super fund fees can eat away at your account balance and stop your super savings from growing as fast as they could. In fact, paying an extra 0.05% p.a. in fees during your working life could reduce your savings by as much as $100,000 when you retire.1

The bottom line

It's important to understand how much you pay in super fees, because it can affect how much money

you'll retire with.

Super fees are what you pay to cover the costs of managing your account (admin fees) and managing the investment option/s your super's invested in (investment fees).

If you're a member, you'll pay admin fees and costs + investment fees and costs and transaction costs.

We deduct your admin fees from your super balance, and you can see them in your transaction history. But you pay investment fees from your investment returns, before we add them to your super balance. This means you won't see these fees show up in your transaction history. But we will show them alongside any other fees you paid on your annual statement.

You might pay other types of fees if you're with a different fund.

At ART, your admin fees cover the regulatory registrations, compliance, tech, marketing, and people costs that help us run the fund and manage members' accounts. Our admin fees and costs are $1.20 per week ($62.40 per year), plus 0.10% p.a. on the first $500,000 of your balance (up to $500 per year). That means the most we'll charge you for admin fees and costs per year per account is $562.40.

At ART, when the admin costs of running the fund are more than what we've collected in admin fees from our members, we'll meet these costs by paying them from our reserves. This means you don't pay this from your account. For the year ending 30 June 2024, we estimated this amount to be 0.07% per account.

This is what we charge to manage each investment option. These fees and costs cover a range of things, such as:

You can see the investment fees and costs and transaction costs we charge for each investment option on our Super fees page.

Good to know: if you're invested in a few different options, you won't pay duplicate sets of investment fees. You'll only pay investment fees on the part of your balance invested in that option.

Our investment fees include performance fees. Other funds might charge these separately.

Transaction costs you'll pay at ART include:

We don't charge buy-sell spreads or switching fees, but other super funds might. They may also include different items in their transaction costs. If you're with another fund, you'll need to check with them.

Some investment option fees can be more than 10 times as expensive than others. Why is that?

The costs of investing in certain types of assets can be a lot higher than others. The costs of professionally managing certain types of investment options can also be much higher. Actively managed options like our Diversified options invest in and trade several asset types (e.g. shares, bonds, property) at once.

Index options, on the other hand, invest in a portfolio that aims to closely match the performance of a market index. Index options are known as 'passively managed' options. They often have lower investment fees than actively managed options.

What matters when looking at fees is to balance them against their investment strategy and the long-term net investment returns they are getting. Cost is just one factor to consider.

Not all the deductions from your super account are super fees. If you've got an account with us and you look at your transaction history, you might notice regular deductions from your account balance:

The Australian Government taxes money contributed to super before tax at a rate of 15%.2 We take this tax from your super and pay it to the ATO. In some cases, you might need to pay more tax.

If you have insurance with us, we'll deduct premiums from your account. Keep in mind you pay insurance premiums for insurance. While we're here, it's important to understand what type/s of insurance you need and how much.

In some cases, you can pay some or all of a financial adviser's advice fees from your super.3

We don't charge any of these fees.

But other funds could charge you fees for activities like switching your investment options. If you're with another super fund, check with them to see if you pay:

Ready to do your own superannuation fees comparison and see how your fund stacks up? Here's how.

If you're an ART member, you can easily see how much you're paying in super fees today by using our super fees calculator. If you're with another fund, and you can't use a calculator to work out your fees, you'll have to work out your admin, investment, and any other super fees you pay manually.

Why do this? It'll help you understand how much you really pay in fees today. This is useful to know before you start comparing benchmarks, which may not represent your financial situation.

The ATO's YourSuper comparison tool uses a benchmark of what someone would pay in super fees if they had a $50,000 balance, and were invested in the fund's MySuper (default) option. Based on this benchmark, our super fees are $507.40 per year.

Remember, the benchmark tool only gives you an estimate, not the actual fees you'd pay with that fund.

Some websites do show superannuation fees comparison tables. But keep in mind that super comparison websites don't always clearly explain what criteria they've used to calculate their results.

Or you can see how much you might pay in fees with ART.

Lower fees are generally a good thing. But low fees might not be worth it if you're not getting good investment returns on your super or good service. On the other hand, what if you're paying more on average in super fees, but your returns are outstanding? Is that a better result?

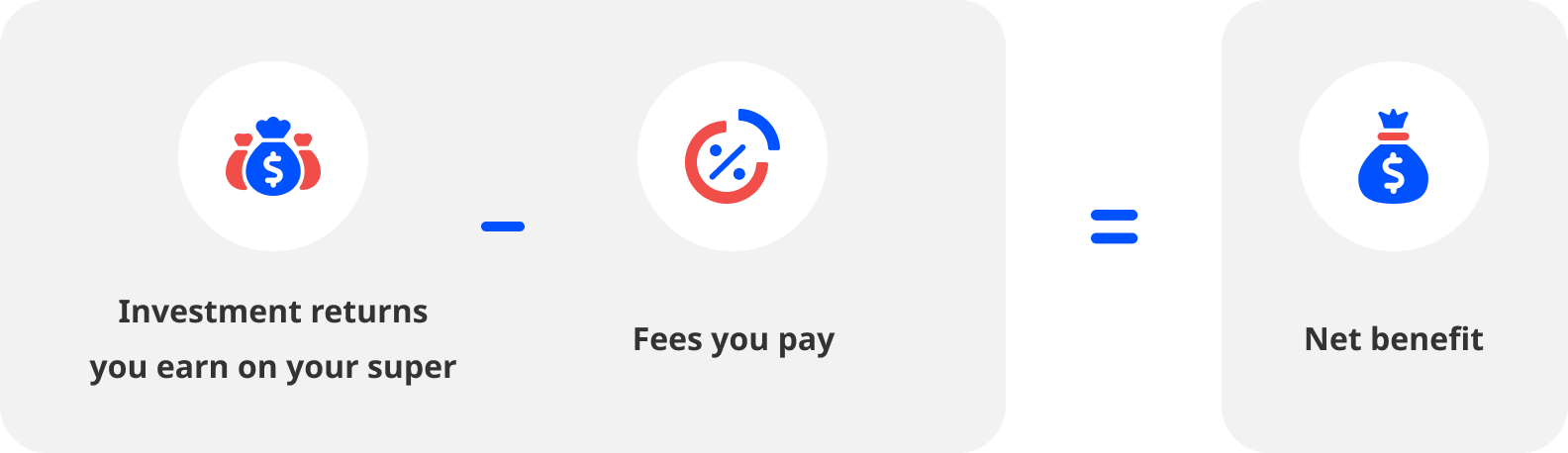

What matters most is how much money gets added to your super on top of your contributions at the end of the day. Or said another way, it's how much money your super makes in investment returns, minus any fees you pay.

We call this amount your net benefit.

Paying higher investment fees might be worth it if the investment returns are high enough that you get a bigger net benefit.

Want to retire in comfort? You're not alone. Here's what to compare when choosing a super fund that's best for you.

6 min read

Ever wondered how a little extra money in your super today could make a big difference tomorrow? It's all thanks to the snowball effect of compound earnings.

2 min read

If you worry about being able to afford the lifestyle you want when you retire, you're not alone. But with our simple tips, you can boost your super and have more for the future.

6 min read

1. Productivity Commission Inquiry Report into Superannuation: Assessing Efficiency and Competitiveness, accessed 20/3/2025 at www.pc.gov.au

2. Understanding Concessional and non-concessional contributions, accessed 21/03/2025 at www.ato.gov.au

3. Financial advice costs, accessed 23/3/2025 at www.moneysmart.gov.au